Sort code: 40-06-21

Account number: 02896109

BIC: HBUKGB4107T

IBAN: GB02HBUK40062102896109

These days, writing a specific article is much easier. Simply ask the AI a specific question, and it (AI) will provide you with the specifics/substantive content of the topic. Then, all you need to do is combine these specific arguments into one border image and its contents, revealing the complexity of this reality.

In that instance POTUS Donald Trump inner circle believes that they are able to distort US President reality perception.

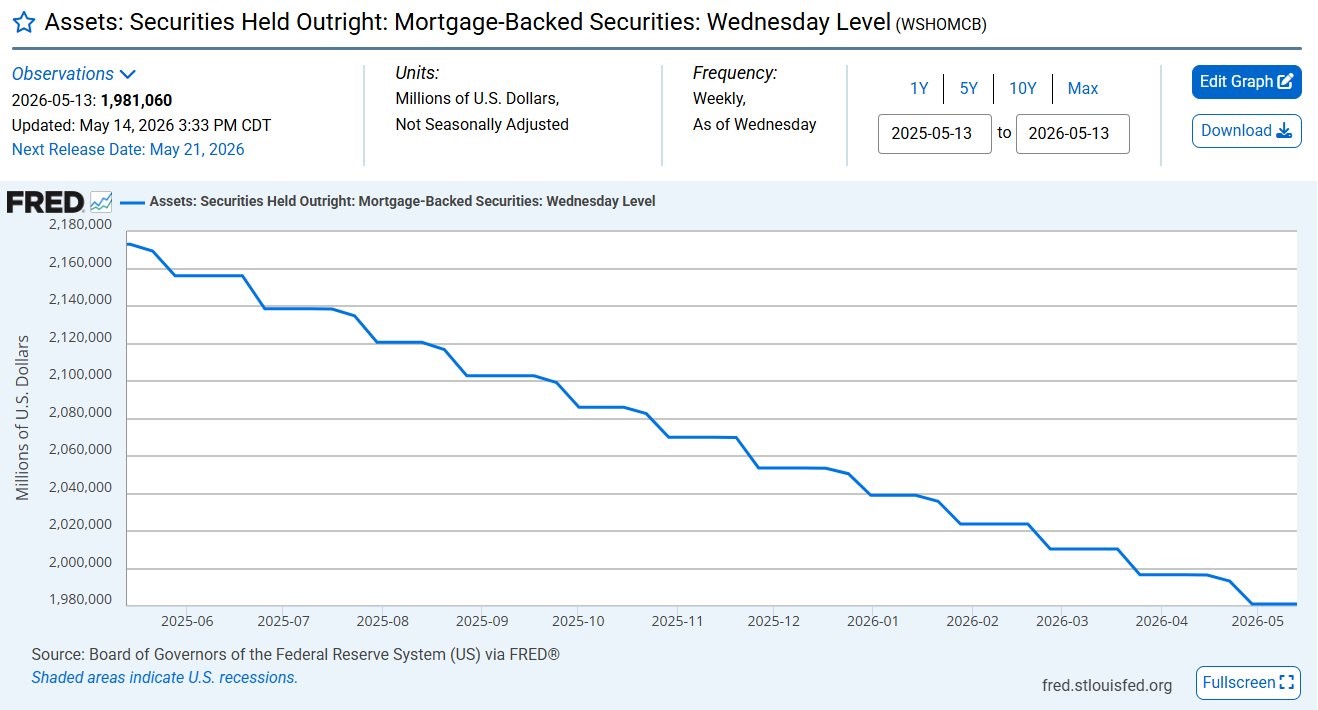

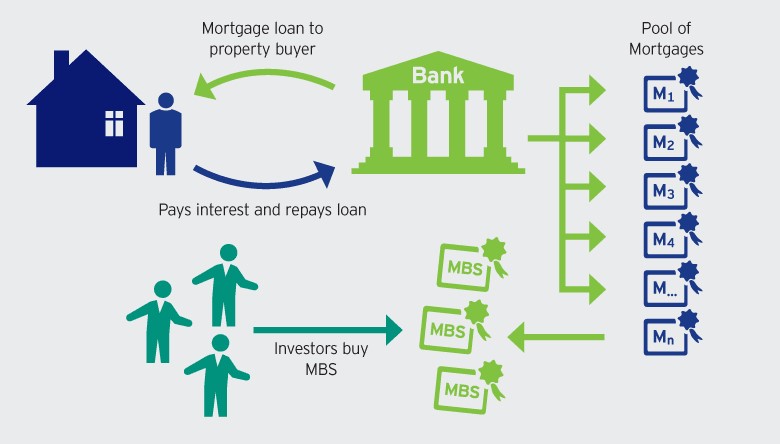

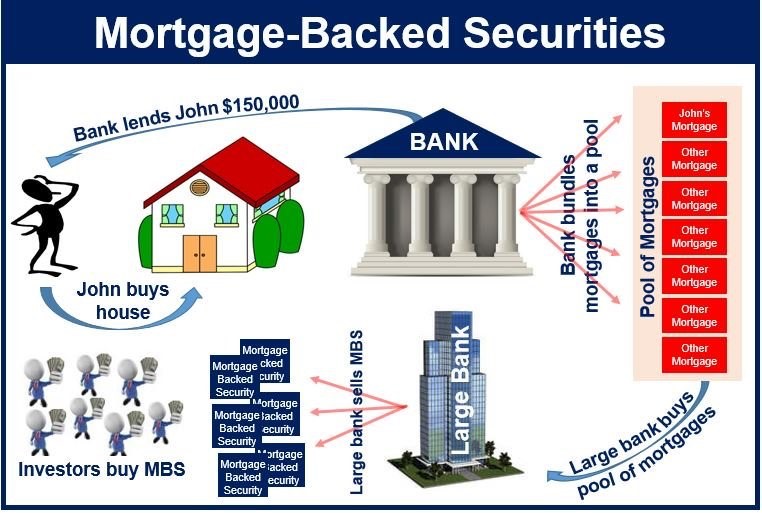

When the U.S. Treasury buys Mortgage-Backed Securities (MBS) from the Federal Reserve, it effectively shifts those assets back to the government while returning cash to the Fed. This reduces the total supply of MBS held by the central bank and alters market liquidity within narrowed part of the market as banking sector. As a Primary Effects we will observe Shift in Asset Ownership. The MBS are moved off the Fed’s balance sheet and will be absorbed by the Treasury, or retired entirely, effectively shrinking the Fed's holdings. … This action operates similarly to Quantitative Tightening (QT). As the Fed sells off or transfers these securities, it absorbs cash and reduces the amount of money circulating in the broader financial system. Interest Rate Adjustments will go by reducing the Fed's footprint in the mortgage market, and upon this maneuver increases the supply of MBS available to private investors. Furthermore, this cause mortgage rates to rise, cooling down a heated housing market. Operational Mechanics Open Market Operations dictate that the Fed typically buys and sells securities to manage the money supply, and the Treasury coordinates with the Fed in executing these transfers. When the Treasury steps in to buy or retire these from the Fed, it restores normal market pricing, leading to higher, more market-aligned mortgage yields and housing costs.

As its immediate outcome upon Treasury (or FED) purchases of Mortgage-Backed Securities (MBS) directly benefit and heavily influence Primary Dealers by acting as an immediate, large-scale buyer in the secondary market. Additionally, as invisible to prime eye such Treasury buy of MBS correct liquidity in financial sector around the GOV auctioned-off coupons and bills. This process expands dealer balance sheets, lowers financing costs, and alters how dealers manage their overall bond portfolios. Mortgage-Backed Securities (MBS) affect Primary Dealers by serving as major drivers of balance sheet usage, risk limits, and liquidity intermediation. Primary Dealers act as the primary middlemen in the Over-The-Counter (OTC) MBS and Treasury markets, meaning the pricing, issuance, and Federal Reserve intervention of MBS significantly shape their operations. MBS activity impacts Primary Dealers in three primary ways:

1. Acting as the Primary Counterparty When the Federal Reserve or Treasury initiates large-scale MBS purchases (e.g., through Quantitative Easing), they execute these daily transactions directly through the Federal Reserve Bank of New York Primary Dealers. Because the government acts as a massive, reliable buyer, dealers are able to quickly offload their MBS inventories, generating immediate liquidity and capturing trading fees.

2. Balance Sheet Constraints & Regulatory Limits MBS positions consume significant capital under regulatory frameworks like the Supplementary Leverage Ratio (SLR) and internal Value-at-Risk (VaR) limits. When MBS market volatility spikes or refinancing waves occur, dealers' risk-bearing capacities are squeezed. To maintain these risk limits, dealers frequently adjust their MBS portfolios, which directly alters their capacity to intermediate and trade other assets (like US Treasuries).

3. Portfolio Balance and Rebalancing Effects When the government buys MBS, it removes significant supply and prepayment risk from the market. This drives up MBS prices and suppresses their yields, forcing private investors to reallocate their capital elsewhere—often into U.S. Treasuries. Inventory Shifts: Primary dealers find themselves acting as market-makers for both MBS and Treasuries. When clients rotate out of MBS and into Treasuries, dealers experience corresponding fluctuations in their net inventory for both asset classes.

4. Monetary Policy Intermediaries When central banks (such as the Federal Reserve) engage in quantitative easing or tightening, Primary Dealers act as the direct counterparties for these MBS transactions. The Fed's purchases and sales of agency MBS require dealers to facilitate trades, balance massive transaction volumes, and absorb market shocks. The initiation or tapering of these operations directly alters dealers' inventory risks and profitability.

5. Balance Sheet Capacity and Constraints Primary dealers are bound by regulatory capital requirements, such as the Supplementary Leverage Ratio (SLR). Cash vs. Forward Contracts: The leverage exposure in the SLR is often based on the notional value of all cash positions. When MBS purchases surge, dealers may find their balance sheets constrained. To manage these limitations, dealers heavily utilize "To-Be-Announced" (TBA) forward contracts and dollar roll operations, effectively delaying or swapping settlements to avoid overloading their balance sheets with spot MBS inventories.

6. Hedging and Portfolio Spillovers Primary Dealers must constantly manage the interest rate risk and prepayment risk embedded in the MBS they hold. When mortgage rates drop, borrowers refinance, which alters the "effective duration" of MBS portfolios held by dealers. To hedge against this, dealers heavily utilize the Treasury and derivatives markets. An increase or decrease in MBS demand triggers major spillover effects on Treasury prices and the broader liquidity that Primary Dealers are obligated to provide. For granular, real-time tracking of Primary Dealer commitments and aggregate MBS cash/forward positions, you can monitor the Federal Reserve Bank of New York Primary Dealer Statistics or read the Federal Reserve's Assessment of Dealer Capacity for detailed insights into dealer constraints.

7. Financing and Repo Market Impacts Primary dealers perform significant maturity transformation by borrowing short-term in the repo market to finance their long-term securities portfolios. Liquidity injection: When the Fed buys MBS, it injects cash directly into the financial system, creating reserves that improve overall liquidity for Primary Dealers in the repo market. Dealers frequently engage in MBS dollar rolls and coupon swaps with the central bank Trading Desk, utilizing these mechanisms to smooth out short-term financing friction and manage their liquidity positions. By functioning as both a massive customer and the ultimate provider of liquidity, MBS purchases ultimately allow Primary Dealers to maintain high trading volumes while carefully maneuvering around strict regulatory capital and risk-assessment constraints.

Knowing all of the above simple question will arise as … What will be the Federal Reserve’s investment strategy for agency MBS going forward?

For example, on August 10, 2010, the FOMC directed the Desk to keep constant the Federal Reserve’s holdings of securities at their current level by reinvesting principal payments from agency debt and agency MBS in longer-term Treasury securities. As a result, agency MBS holdings will decline over time. Any future decisions about the investment strategy to be employed will be made by the Federal Open Market Committee.

So, when the U.S. Treasury buys Mortgage-Backed Securities (MBS) from the Federal Reserve, it directly replaces the Fed's housing debt with cash. This action shrinks the Fed's balance sheet, reduces the private market's MBS supply, and functions as an intervention to manage housing affordability. Such effect can be achieved either upon raise the interest rates or key mechanics and impacts of this process that will include. The Treasury steps in to purchase MBS directly from the Fed’s portfolio, often to match the Fed's monthly runoff or quantitative tightening (QT) caps, helping stabilize the secondary mortgage market. Balance Sheet Dynamics as the Fed’s holdings of MBS decline, removing those mortgage assets from its System Open Market Account (SOMA) portfolio. Additionally, by absorbing these securities, the Treasury limits the supply that would otherwise need to be absorbed by private buyers, helping to put downward pressure on the spread between mortgage rates and Treasury yields. These strategic buybacks—like those initiated to counter housing affordability issues—inject stability into the mortgage market, supporting the operations of government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac.

And this is not all because when the U.S. Treasury buys Mortgage-Backed Securities (MBS) directly from the Federal Reserve, it reduces the supply of MBS in the market while transferring cash to the central bank. This inter-agency transaction generally results in the following immediate effects as debt Restructuration because the Federal Reserve’s balance sheet shifts from holding private-labeled or agency MBS to holding cash, while the Treasury effectively brings those mortgage-backed assets into the government's financial umbrella. Additionally, it makes Interest Rate Stabilization within GOV securities operators. By purchasing MBS, the Treasury absorbs some of the market risk associated with bundled mortgages. This can compress the spread between mortgage rates and Treasury yields, helping to stabilize housing finance costs. No Direct Impact on Broad Money Supply: Unlike when the Fed buys securities (which injects new reserves into the banking system to stimulate the economy), a direct Treasury-to-Fed purchase is an asset swap between two government entities. It does not directly print new money or alter the total amount of currency circulating in the public economy. Capital Remittance Adjustments: The Fed regularly remits its net profits to the U.S. Treasury. Trading or holding these MBS will alter the Fed's profitability, ultimately affecting the net income transferred back to the government at the end of the fiscal year.

Because as immediate effect that will shift the liquidity from the market to Treasure operators, we do see the private credit "crisis" refers to mounting stress within the $2 trillion direct-lending market, driven by high-profile defaults, a software industry downturn, and a surge in investor redemption requests. While regulators see parallels to the 2008 financial crisis, it is widely viewed as an illiquidity crunch rather than a systemic meltdown. Key Market Stresses Rising Defaults with high interest rates and heavy exposure to the software sector (which is vulnerable to AI disruption) have made it difficult for smaller, leveraged companies to service their loans. It is also Fund Gating as Investors—particularly retail and semi-liquid vehicle investors—attempting to withdraw their capital are increasingly facing withdrawal limits. Funds restrict redemptions to prevent fire sales of inherently illiquid assets. Valuation Doubts that will comes as funds are marked down, doubts have surfaced regarding whether previous stated Net Asset Values (NAVs) were accurate, prompting more investors to request their money back. Officials like the Bank of England's Sarah Breeden warn of concerning echoes from the 2008 crisis. These include opaque interconnectedness between banks, insurers, pension schemes, and the rapid, untested growth of the sector. Major asset managers like BlackRock and Apollo maintain that the systemic threat is low. Unlike the 2008 subprime mortgage crisis, the leverage involved in private credit is generally low (typically 2 to 1), and inherent default risks are mostly acknowledged by institutional participants. Asset management giants—including KKR, BlackRock, and Apollo Global Management—are actively buying back or restructuring troubled funds to address reputational stains and restore investor confidence. To dive deeper into the specific metrics of the private credit market or review sector analyses, you can check insights from institutional leaders such as the Goldman Sachs Top of Mind Report or listen to recent coverage on the BBC Big Boss Interview regarding the Bank of England's ongoing scrutiny of the sector.

As of mid-2026, the private credit market is experiencing significant stress, characterized by rising defaults (roughly 5.8%-9%) and high redemption pressures, rather than an abrupt, total system collapse. Major lenders are enforcing withdrawal caps to manage a "liquidity mirage," as high-interest rates and reliance on PIK toggles strain borrower cash flows. Key 2026 Private Credit Pressures that Rising Defaults and Distress for example Fitch Ratings reported a 5.8% US private credit default rate through January 2026, the highest on record. Other reports suggest accelerated stress reaching 8-9%, with projections for further increases due to a "maturity wall". Liquidity Strain ("Liquidity Mirage") comes as major funds like BlackRock, Blackstone, and Blue Owl have enforced quarterly redemption caps, with requests far exceeding capacity. Increased reliance on payment-in-kind (PIK) interest—where interest is paid in more debt rather than cash—indicates borrower distress. The Financial Stability Board (FSB) warned of high exposure to tech, healthcare, and AI infrastructure loans, where rapid valuation increases in 2025 are facing corrections in 2026.2026 Maturity Wall: 23 of 32 rated Business Development Companies (BDCs) face unsecured debt maturities totaling $12.7 billion, a 73% increase over 2025 levels. While not an immediate meltdown, the market is undergoing a painful maturation, favoring distress specialists over generalist lenders. The surge in 2025 AI-focused investments is expected to lead to sizeable credit losses.

By Peter von Roggenhausen May 19 2026.

Ps. I'm very sorry for the slow action on posting the news; The reason as usually if the fund. We so far did not receive any single penny or red cents in donation. This means that our expenses are covered from the fund we have and loan we have obtain. I have heard some rumors about the donation you have made to US but I can ensure you that such never get to US. So, since we do not accept rumors if you have made any donation ask your band as where it get to? Because we have not received it. Or you can send to US a copy of the donation and we will trace it on your behalf.

Oh. Well, as the people saying "Money talks" ... so if we had had the necessary fund, you will have the right information at the right time.

Sort code: 40-06-21

Account number: 02896109

BIC: HBUKGB4107T

IBAN: GB02HBUK40062102896109